U.S. Treasuries sold off hard Thursday, with the two-year rising 24 basis points to hit above 1.60%, the five-year inching closer to 2% and the 10-year UST surpassing 2%, after inflation hit a four-decade high at 7.5%. Municipals followed suit, rising by five to eight basis points, but dramatically outperformed USTs.

Equities took a beating, particularly tech stocks as markets digested a likely more hawkish Fed next month.

While the consumer price index report raises the possibility of a 50-basis point hike in March, it “is not a foregone conclusion,” said Jas Thandi, partner of portfolio strategy at Aon.

By raising 50 basis points in March, the Fed would show markets it “is serious about getting inflation under control,” Thandi said, and may “give the Fed the ability to create some breathing space to see how the second quarter plays out, before embarking on more rate hikes.”Understanding credit ratingsMoody’s Investors Service is a leading global provider of credit ratings, research and risk analysisPARTNER INSIGHTS

MOODY’S

The downside is a possible negative market reaction, but if a 50 basis-point liftoff is expected, he said, “markets should not react much.” The key is to avoid surprises and “the guidance around such a hike will be critical,” Thandi added.

Triple-A muni benchmark yields were cut by up to eight basis points on the short end but the pain was felt across the curve with cuts of up to five seen out long. The municipal to UST ratio five-year was at 64%, 75% in 10 and 85% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 64%, the 10 at 78% and the 30 at 85% at a 4 p.m. read.

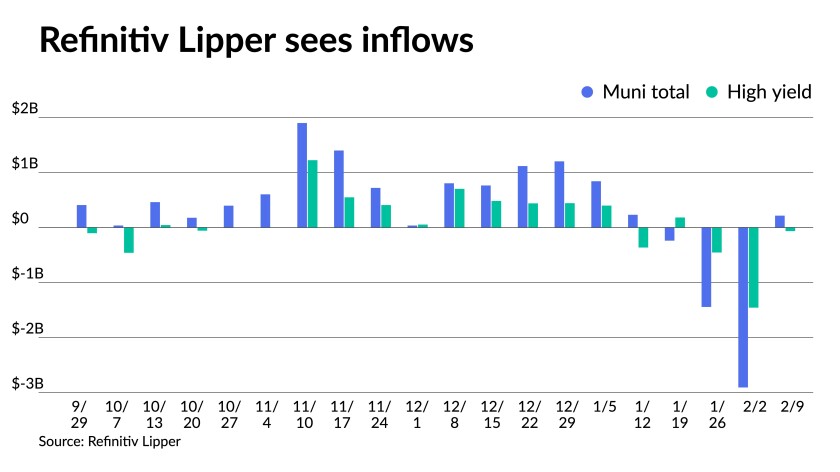

A somewhat bright spot came from Refinitiv Lipper reporting inflows into municipal bond mutual funds in the latest reporting week to the tune of $216 million following three weeks of large outflows. High-yield saw smaller outflows while exchange-traded funds reported $755 million of inflows.

Lower supply also may be a factor that will keep munis outperforming Treasuries for the time being, noted Refinitiv MMD’s Peter Franks.

Thirty-day visible supply ticked up to $8.41 billion — still a rather low figure for a month out — while net negative supply is at $9.957 billion, with the largest deficits from Texas and New York issuers.

Indeed, many deals have moved to the day-to-day calendar amid the market volatility with Ohio earlier this week pulling its $400 million-plus taxable deal, a not so surprising move given the rate increases and taxable munis lagging a rebound in performance.

Customer selling continues to weigh on the dealer community, according to Michael Pietronico, chief executive officer at Miller Tabak Asset Management. Bids wanteds hit $1.4 billion on Wednesday after $1.35 billion on Tuesday.

“Longer maturity bonds will see the most pressure in our view as institutional accounts try to reduce duration in front of a Federal Reserve tightening cycle,” he said on Thursday.

Few deals were priced in the primary Thursday. Citigroup Global Markets priced for the Industrial Development Authority of the County of Maricopa, Arizona (Ba2/BB+/BB+/) $145.06 million of exempt facilities revenue bonds, Series 2022. Bonds in 10/2047 with a 4% coupon yield 3.5%, callable 1/1/2026.

In the competitive market, the University System of Maryland (Aa1/AA+/AA+/) sold $102.895 million of auxiliary facility and tuition revenue bonds, 2022 Series A, to J.P. Morgan Securities. Bonds in 4/2023 with a 5% coupon yield 0.70%, 5s of 2027 at 1.31%, 5s of 2032 at 1.66%, 3s of 2037 at 2.27%, 3s of 2042 at 2.43%, 3s of 2047 at 2.61% and 3s of 2052 at 2.71%, callable in 4/1/2032.

The University System of Maryland (Aa1/AA+/AA+/) also sold $23.525 million of auxiliary facility and tuition refunding revenue bonds, 2022 Series B, to J.P. Morgan Securities. Bonds in 4/2023 with a 5% coupon yield 0.70% and 5s of 2026 at 1.23%, noncall.

Secondary trading

Georgia 5s of 2023 at 0.74%. Maryland 5s of 2023 at 0.80%. Minnesota 5s of 2023 at 0.85%. Fairfax County, Virginia 5s of 2023 at 0.77%-0.76%. Hawaii 5s of 2023 at 0.72%.

Wisconsin transportation 5s of 2026 at 1.29%. New York City 5s of 2026 at 1.40%. California 5s of 2027 at 1.51%-1.40%. NYC TFA 5s of 2027 at 1.47%-1.46%.

University of Texas 5s of 2031 at 1.60%. California 5s of 2032 at 1.70% versus 1.48% last Friday.

LA DPW 5s of 2040 at 1.98% versus 1.83% on Monday.

NYC TFA 5s of 2047 at 2.25% versus 2.24% Wednesday. Triborough Bridge and Tunnel Authority 5s of 2047 at 2.30%-2.29% versus 2.25% Wednesday.

AAA scales

Refinitiv MMD’s scale saw were cut five basis points across the curve at the 3 p.m. read: the one-year at 0.68% (+5) and 0.95% (+5) in two years. The five-year at 1.24% (+5), the 10-year at 1.53% (+5) and the 30-year at 1.96% (+5).

The ICE municipal yield curve saw the largest cuts to its short end: 0.69% (+8) in 2023 and 1.00% (+7) in 2024. The five-year at 1.24% (+6), the 10-year was at 1.59% (+6) and the 30-year yield was at 1.97% (+5) in a 4 p.m. read.

The IHS Markit municipal curve was cut: 0.68% (+4) in 2023 and 0.92% (+5) in 2024. The five-year at 1.26% (+5), the 10-year at 1.53% (+6) and the 30-year at 1.96% (+5) at a 4 p.m. read.

Bloomberg BVAL was cut three to five basis points: 0.70% (+3) in 2023 and 0.93% (+4) in 2024. The five-year at 1.27% (+4), the 10-year at 1.54% (+4) and the 30-year at 1.95% (+5) at a 4 p.m. read.

Treasuries sold off while equities ended in the red.

The two-year UST was yielding 1.612% (+24), the five-year was yielding 1.969% (+15), the 10-year yielding 2.051% (+10), the 20-year at 2.395% (+8) and the 30-year Treasury was yielding 2.313% (+6) at the close. The Dow Jones Industrial Average lost 526 points or 1.47%, the S&P was down 1.81% while the Nasdaq lost 2.10% near the close.

Inflation continues

The consumer price index showed inflation at rates not seen since the 1980s and were higher than expected, with headline and core gaining 0.6% in January, with the annual rate up 7.5% and the core up 6.0% in that time.

“Today’s data coupled with the resilience of hiring through the Omicron wave in January means the Fed has to abruptly hit the brakes which increases the risk of a misstep,” said Grant Thornton Chief Economist Diane Swonk.

“Inflation not only remains high, but it continues to accelerate,” said Steve Chiavarone, head of multi-asset solutions at Federated Hermes. “With owners’ equivalent rent and energy prices both likely to trend higher in the coming months, it does not look like we are yet close to an inflection point.”

The Federal Reserve may need to raise rates six or seven time this year, he said. “It will be interesting to listen to Fed speak to see if they take any steps towards endorsing a 50 bp move at any point.”

But the Fed plays a long game. “A critical question is how the Fed and markets respond if, as we expect, inflation moderates through 2022 but remains significantly above the Fed’s inflation forecast,” said Berenberg Capital Markets Chief Economist for the U.S. Americas and Asia Mickey Levy.

After CPI was released, he noted, the futures market started pricing in four rate hikes by July.

The report suggested “everything got more expensive in January,” said Edward Moya, senior market analyst at OANDA, “and fears remain that it will get worst.”

Rents, electricity, energy and food all continue rising, he noted.

“The Fed will be tested here as they were hoping to have a gradual tightening cycle and not a mad dash that looks like a policy mistake,” Moya said. “With core inflation well above the Fed’s target and real average hourly earnings declining, the political pressure will also grow on the Biden administration and Democrats. November is still far away, but this inflation report is showing price increases are everywhere and resistance is growing for more fiscal packages that will fuel further pricing pressures.”

The Fed fight against inflation is late, said Cato Senior Fellow and Director Emeritus of the of the Center for Monetary and Financial Alternatives George Selgin. Consumer spending surpassing pre-COVID rates by last November, he said, “warranted a Fed response, supply bottlenecks and all that notwithstanding. Three months later, we’re still waiting for it, and inflation rages on.”

But just the expectation of Fed rate hikes and balance sheet reduction has prompted tightening, noted Ron Temple, head of U.S. Equities at Lazard Asset Management.

“Markets aren’t waiting for the Fed, as financial conditions are tightening already across developed markets,” he said. Although no real surprises emerged from CPI, when taken with recent employment data, “it dials up the pressure on the Fed to act. It’s imperative for the Fed to moderate its hawkish instincts recognizing that growth and price pressures are likely to abate and unemployment to trough even without tightening as we enter the second half.”

A 50-basis point hike would be overkill, he said. “The Fed needs to signal a commitment to controlling inflation, but it also should look beyond the first quarter peak in inflationary pressure that is forecast by many economists.”

GDP and inflation should slow and unemployment may rise as people return to the workforce, Temple noted. “These developments are likely to mitigate the arguments for a more hawkish approach.”

While the odds of a bigger liftoff have gone up, he said, “the Fed should exercise caution to ensure it does not destabilize markets by catering to the wants of the most hawkish commentators. The combination of the end of asset purchases and a 25 bp hike is sufficient in my view to reaffirm the Fed’s inflation fighting credentials.”

While a bigger increase would show the Fed’s willingness to be aggressive against inflation, if needed, “a 50 bp hike could also alarm investors by indicating that the Fed believes it is actually behind the curve.”

And, the extra quarter point “does not materially affect inflation,” Temple said. “It’s more of signal to affect market psychology.”

By taking a “measured” approach that allows it to see and “understand the impact of each policy move before making the next,” he said, the Fed can achieve its dual mandate.

And while the market appears ready for either move, the Fed still will receive two labor reports and another inflation report before its March meeting, Temple said. “By mid-March, the decision regarding the pace of policy tightening may well be an easier one.”

The higher-than-expected readings raise the specter of a 50-basis point liftoff in March, said John Farawell, managing director and head of municipal trading at Roosevelt & Cross. “The challenge for the Fed to curb inflation and leave the economy with a soft landing seems arduous.”

Still others are looking longer term. “While prices continue to rise at elevated rates, we’re starting to see signs that record-setting inflation won’t be with us much longer,” observed John Leer, Morning Consult’s chief economist. “Math is also on the side of driving down 12-month inflation. As we move into the second quarter of the year, we’ll be comparing prices with the already-elevated levels from last spring, meaning the change in prices relative to last year won’t be as large.”

Also, he noted, consumer demand won’t grow as much as it did in 2021, which should curb inflationary pressures.

David Kelly, chief global strategist at J.P. Morgan Asset Management, agreed. “We still believe that inflation will begin moderating soon.” But, he added, the Fed still has “a lot of work to do.”

The Fed futures are now pricing in more than a 50% chance of a half-point rate hike in March, he said, “and 10-year yields rose to hover just below 2%.”

While he doesn’t expect inflation to hurt economic growth, Kelly said, “a chronic shortage of labor might soon act as a real constraint on the economy. In this environment, an over reactive Fed that starts tightening too much and too fast might mean that we end the year with much slower growth to accompany lower inflation.”

Mutual funds see inflows

In the week ended Feb. 9, weekly reporting tax-exempt mutual funds rebounded, with Refinitiv Lipper reporting Thursday $215.512 million of inflows. It followed an outflow of $2.906 billion in the previous week, the largest negative flows in nearly two years.

Exchange-traded muni funds reported inflows of $754.758 million after inflows of $62.53 million in the previous week. Ex-ETFs, muni funds saw outflows of $539.246 million after $2.969 billion of outflows in the prior week.

The four-week moving average fell to negative $1.09 billion from negative $1.087 million in the previous week.

Long-term muni bond funds had inflows of $222.678 million in the last week after outflows of $1.982 billion in the previous week. Intermediate-term funds had outflows of $86.388 million after $294.395 million of outflows in the prior week.

National funds had inflows of $297.247 million after outflows of $2.968 billion the previous week while high-yield muni funds reported $65.586 million of outflows after $1.456 billion of outflows the week prior.

Informa: Money market muni funds rise

Tax-exempt municipal money market fund assets rose by $65.9 million, bringing their total to $85.8 billion for the week ending Feb. 7, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 150 tax-free and municipal money-market funds remained at 0.01%.

Taxable money-fund assets lost $31.98 billion, bringing total net assets to $4.458 trillion in the week ended Feb. 7. The average seven-day simple yield for the 780 taxable reporting funds was steady at 0.01% from a week prior.

Original Source: https://www.bondbuyer.com/news/munis-vastly-outperform-massive-ust-selloff