Municipals were little changed and lightly traded Monday as the market readies for the new month and lighter supply this week while all eyes remain on Wednesday’s FOMC meeting.

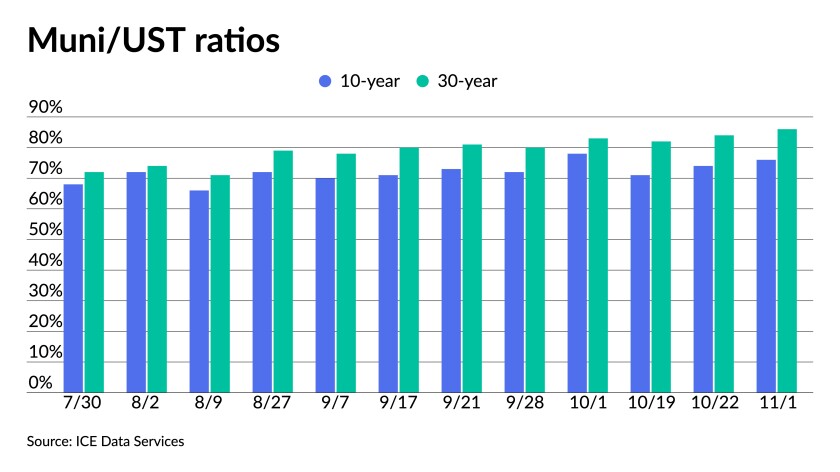

Triple-A benchmarks were little changed on Monday while ratios hovered near recent levels. Municipal-to-UST ratios saw the 5-year at 53%, the 10-year at 76% and the 30-year at 86%, according to ICE Data Services.

November is likely to be more volatile than October. Though monetary policy has been in the forefront, at mid-month the tone changed with global inflation outlooks and federal infrastructure and social package in flux, noted Kim Olsan, senior vice president at FHN Financial.

“What the market thought was a path toward higher individual and corporate rates has turned more suspect and brings into question how much additional demand may develop (or current inquiry be sustained),” she said. These factors combined to create weakness across most municipal sectors last month.Bond Buyer Advances in Tech Demo EventDPCDATA, MSRB, IHS MARKIT

Despite low yields, she said defensive duration allotments paid off last month. Short-term bonds ended flat in October, outperforming intermediate and long bonds by 30-40 basis points. However, earlier gains out the curve have both 10- and 30-year-range bonds up 1.25% to 2% on the year. A curve slope of about 150 basis points will hold enough lure for inquiry stretching past short-term bonds to reach hard yield or taxable equivalent yield targets.

Taxable munis were helped by a UST rally, earning 0.39% last month and sitting with a near-1% gain for the year, she said. Issuance totaled $12 billion per Bloomberg data, well off last year’s election-driven surge but ahead of the yearly pace of $9.7 billion.

The luster of high yield is coming down, and “recent fund flows suggest buyers have turned more cautious on the category, perhaps realizing credit spreads have gone about as far as they can,” Olsan said.

Long municipal yields ended the week slightly lower, although less than long Treasuries, noted John Miller, head of municipals and Anders Persson, CIO of fixed income at Nuveen.

“Municipal yields will have a hard time moving substantially lower through the end of the year, as new-issue supply will likely remain outsized,” they said. “We expect both municipal and Treasury rates to remain range-bond in the near term. Beginning in January, we should have a better idea of whether the economy has fully recovered from the pandemic.”

Miller and Persson also noted the high yield and AAA-rated municipal bond yields decreased evenly by 4 basis points on average last week.

“Cross currents in high yield municipal fund flows were evenly balanced, with net flows of $3 million. High-yield municipal new issuance remains active, with at least 30 deals this coming week,” they said.

The Puerto Rico Oversight Board’s announced last week that it accepted recently passed legislation clearing the way to finish restructuring the island’s debt and Miller and Persson pointed to an upcoming $60 million Puerto Rico hospital deal as a positive signal for the territory.

“An old and once-popular Puerto Rico credit — Auxilio Mutuo Hospital — returns to the market this week, a sign that market access is returning to Puerto Rico credits that were blocked due to its bankruptcy proceedings,” they wrote.

Puerto Rico’s general obligation bonds traded up last week after the board announced the deal with 8s of 2035 trading as high as $88.125 Monday, up from $86.250 and $86.000.

In the primary Monday, BofA Securities priced for retail for the State Public Works Board of the state of California (Aa3/A+/AA-/) $574.46 million of lease revenue bonds, consisting of $475.245 million of Department of General Services climate bond certified green bonds. Bonds 11/2022 with a 5% coupon yield 0.19%, 5s of 2026 at 0.73%, 5s of 2031 at 1.37%, 4s of 2041 at 2.17% and 5s of 2046 at 2.00%, callable Nov. 1, 2031.

The second tranche, $99.215 million of various capital projects lease revenue bonds, with 4s of 11/2022 at 0.19%, 4s of 2026 at 0.73%, 4s of 2031 at 1.37%, and 2.5s of 2046 at 2.64%, callable in Nov. 1, 2031.

Secondary trading

Georgia 5s of 2022 at 0.11%. Florida 5s of 2022 at 0.18%. Stanford 5s of 2023 at 0.21%.

Cincinnati 5s of 2024 at 0.45% versus 0.35% original. Connecticut 5s of 2026 at 0.64%-0.62%. Arlington County 5s of 2027 at 0.76% versus 0.77% Friday.

New York City TFA 5s of 2031 at 1.39%-1.38%. Michigan Trunkline 5s of 2033 at 1.43%. Texas water 5s of 2034 at 1.42%. Ohio water 5s of 2035 at 1.44% versus 1.47% Thursday.

Los Angeles DWP 5s of 2051 at 1.78%. Triborough Bridge & Tunnel 5s of 2051 at 2.02%.

AAA scales

According to Refinitiv MMD, yields were increased for the October to November roll. The one-year rose one to 0.16% in 2022 and at stayed at 0.25% in 2023, the 10-year rose one due to roll to 1.22% and the yield on the 30-year sat at 1.69%.

The ICE municipal yield curve showed bonds steady at 0.17% in 2022 and at 0.25% in 2023. The 10-year maturity was steady at 1.18% and the 30-year yield sat at 1.69%.

The IHS Markit municipal analytics curve showed short yields steady at 0.16% in 2022 and at 0.23% in 2023. The 10-year yield was at 1.24% and the 30-year yield at 1.70%.

The Bloomberg BVAL curve showed short yields steady at 0.17% in 2022 and steady at 0.21% in 2023. The 10-year yield was steady at 1.21% and the 30-year sat at 1.72%.

In late trading, Treasuries were mixed and equities were up near the close.

The 5-year Treasury was yielding 1.189%, 10-year Treasury was yielding 1.567%, the 20-year at 1.996% and the 30-year Treasury was yielding 1.962%. The Dow Jones Industrial Average rose 94 points, or 0.26%, the S&P was up 0.07% while the Nasdaq gained 0.52%.

Fed fears

Despite the certainty the Federal Open Market Committee meeting will end with a taper announcement, some concern remains.

“No matter what, the Fed is going to need to thread the needle very carefully this week given recent bond market dynamics,” said John Hancock Investment Management’s co-chief investment strategists Emily Roland and Matt Miskin. “A flattening yield curve is a problem for the Fed, as it limits the amount of tightening they can do without inverting the curve — a classic harbinger of recessions,” they said. “However, if the Fed stays on the sidelines for too long, inflation may get out of hand.”

The latest data, showing high inflation, lower incomes and continued consumer spending, “may further complicate the FOMC’s decision process,” said Robert Eisenbeis, vice chairman and chief monetary economist at Cumberland Advisors.

“Regardless of the measure used, the Fed finds itself confronting inflation that at this point … is difficult to characterize as transitory,” he said.

And transitioning monetary policy is never easy. “The Fed does not sport a stellar record of policy transitions and this week’s meeting will be met with some trepidation,” said Daniela Mardarovici, co-head of us multisector fixed income at Macquarie Asset Management.

Federal Reserve Chair Jerome “Powell is faced with the difficult task, especially when observed by markets through a microscope, of acknowledging inflation pressures while reassuring markets that the Fed will not stifle the demand recovery in its infancy,” she said.

Recent data suggest the possibility of stagflation grew, Mardarovici said. “And while the Fed has been historically adept at managing rising inflation, it is not well-equipped to manage supply-side pressures in an era of fragile and woefully unequal economic growth.”

Expect “an overhaul” of the post-meeting statement, according to Morgan Stanley Research. The committee will offer more guidance on inflation, they said, which “will require a substantial rewrite of the statement.”

During his press conference, they said, “Powell is likely to continue to stress that liftoff remains far off.”

Grant Thornton Chief Economist Diane Swonk agrees, “the FOMC will have to address the thorny issue of inflation in its statement on policy.” That could take the form of “removing the word ‘transitory.’”

While she believes taper will begin with a $15 billion reduction, “the Fed could accelerate the tapering process if necessary to get to liftoff sooner; that is looking more probable,” she said.

This, despite slowing inflation. “It may not slow fast enough to become insignificant for the public,” Swonk said. “The reason the Fed has a 2% target on inflation is because few struggle to deal with prices moving up too rapidly or falling too quickly when overall inflation is close to 2%.”

If COVID becomes a major issue again, the economy could take another hit, and that would change the Fed’s thinking, she added.

But despite the high levels of inflation, Greg McBride, chief financial analyst at Bankrate, noted, “much can change in the months ahead. Economic growth, employment, financial stability, and geopolitical concerns are all variables that will come into play in addition to inflation.”

Despite a weak GDP report and slowing labor growth, John Farawell, managing director and head of municipal trading at Roosevelt & Cross, said, the Fed won’t delay taper.

“The GDP number, unemployment, and the slight inversion of the 20 year and 30-year UST bond hints at a not so vibrant economy,” he said. “So the taper should occur as scheduled but the Fed raising rates soon seems unlikely. The question is inflation really transitory also adds to the Fed’s dilemma.”

Two scenarios exist for taper, according to Ed Al-Hussainy, senior interest rate and currency analyst at Columbia Threadneedle Investments. The generally expected $15 billion to $20 billion monthly reduction in asset purchases beginning this year and ending by June, or a faster taper allowing rate hikes earlier in 2022.

Under the first possibility, the Fed would emphasize “inflation/labor market thresholds for hikes remain high,” he said. If this occurs, expect a “steeper [yield] curve, lower front end rate volatility, [and] pain concentrated in longer end, higher [break even]s.”

Should the Fed hasten taper, the statement will emphasize “inflation momentum is likely to require a Fed response,” Al-Hussainy said, leading to “a flatter curve, pain concentrated in 2-5 year sector, elevated front end rate volatility, higher real rates, lower BEs.”

Strong earnings and other data offset the weakness in the employment report, said Peter Cramer, senior managing director and head of insurance portfolio management at SLC Management. “Long real yields and inflation expectations appear to disagree with the signals emanating from the front end of the curve,” he said. “30-year real yields are lower month to date and are now near their all-time lows, which is historically inconsistent with an imminent taper.”

And while risks of a policy mistake “tend to increase as greater hawkishness enters the forecast,” Cramer said, “not this time. Despite aggressive hikes getting priced in, the Fed’s 5y/5y — which is a calculated level of inflation expectations for a five-year period that begins five years from today — moved higher.”

His takeaway? “While tapering remains on track, the road to rate hikes remains treacherous.”

In data released Monday, the Institute for Supply Management’s manufacturing index dipped less than expected, registering 60.8% in October, down from 61.1% in September.

Economists polled by IFR Markets expected a drop to 60.5%.

The prices index gained in the month.

“Meeting demand remains a challenge, due to hiring difficulties and a clear cycle of labor turnover: As workers opt for more attractive job opportunities, panelists’ companies and their suppliers struggle to maintain employment levels,” said Timothy R. Fiore, chair of the ISM’s manufacturing business survey committee.

Separately, construction spending dropped 0.5% in September after a 0.1% rise in August.

Economists expected a 0.4% increase.

Primary to come

The Texas Public Finance Authority (/AAA/AAA/) is set to price Tuesday $831.365 million of state of Texas general obligation and refunding bonds, consisting of $248.655 million, Series 2021A, serials 2022-2039 and $582.71 million, Series 2021B, serials 2022-2041. Raymond James & Associates.

Main Street Natural Gas (Aa2//AA-/) is on the day-to-day calendar with $750 million of gas supply revenue bonds, Series 2021A, serials 2023-2031, term 2052. RBC Capital Markets.

Beth Israel Lahey Health (A3/A//) is set to price Wednesday $500 million of taxable bonds, Series L (2021). Goldman Sachs & Co.

Allina Health System (Aa3/AA-/AA-//) is set to price Thursday $303.031 million of corporate CUSIP taxable bonds, Series 2021. J.P. Morgan Securities.

The Economic Development Authority of Lynchburg, Virginia, (Baa1/A-/A-/) is set to price Thursday $211.955 million of hospital revenue and refunding bonds (Centra Health Obligated Group), Series 2021, serials 2027-2047 and 2049-2055. Barclays Capital.

Idaho Health Facilities Authority (A3/A///) is set to price Tuesday $211.885 million of revenue bonds, Series 2021A (St. Luke’s Health System Project). J.P. Morgan Securities.

Minneapolis, Minnesota, (Aa3/AA-/AA-//) is set to price Thursday $172.135 million of health care system revenue bonds, Series 2021 (Allina Health System). J.P. Morgan Securities.

The North Dakota Housing Finance Agency (Aa1///) is set to price Tuesday $141.3 million of housing finance program bonds (Home Mortgage Finance Program), consisting of $125 million, Series 2021B (non-AMT) (social bonds), serials 2027-2033, terms 2036, 2041, 2043 and 2052 and $16.3 million, Series 2021C (AMT) (social bonds), serials 2022-2027. RBC Capital Markets.

The Fort Bend Grand Parkway Toll Road Authority, Texas, (Aa1//AA+/) is set to price Thursday $137.16 million of limited contract tax and subordinate lien toll road revenue refunding bonds, Series 2021A. Mesirow Financial.

The Regents of the University of Colorado (Aa1//AA+//) is set to price Tuesday $136 million of university enterprise refunding revenue bonds, consisting of $68 million, Series 2021C-3A (term rate bonds) (green bonds) and $68 million, Series 2021C-3B (term rate bonds) (green bonds). Loop Capital Markets.

Palm Beach County Health Facilities Authority, Florida, is set to price $128.815 million of revenue refunding bonds (Toby & Leon Cooperman Sinai Residences at Boca Raton), Series 2022 (forward delivery). HJ Sims & Co.

The Successor Agency to the Redevelopment Agency of the City and County of San Francisco (/AA///) is on the day-to-day calendar with $107.34 million of taxable third-lien tax allocation bonds, 2021 Series A (affordable housing projects) (social bonds), serials 2023-2031, insured by Assured Guaranty Municipal Corp. Citigroup Global Markets.

Spartanburg Regional Health Services District, South Carolina, (A3/A//) is set to price Wednesday $101.895 million of hospital revenue refunding bonds, Series 2022 (forward delivery). J.P. Morgan Securities.

Puerto Rico Industrial, Tourist, Educational, Medical and Environmental Control Facilities Financing Authority (/BBB+//) is set to price Tuesday $60.005 million of hospital revenue and refunding revenue bonds, Series 2021 (Hospital Auxilio Mutuo Obligated Group Project). J.P. Morgan Securities.

Competitive

Washington (Aaa/AA+/AA+) is set to sell $133.665 million of unlimited tax general obligation bonds at 11 a.m. eastern Tuesday. The state will also sell $134.545 million of motor vehicle fuel tax general obligation refunding bonds, Series R-2022B at 11:30 a.m. eastern Tuesday.

Miami-Dade County School District (Aa3///) is set to sell $169.08 million of taxable general obligation school refunding bonds, Series 2021 at 10 a.m. eastern Wednesday.

Dallas, Texas (///AA+) is set to sell $235.245 million of unlimited tax general obligation bonds at 10:30 a.m. eastern on Thursday.

Jessica Lerner contributed to this report.

Original Source: https://www.bondbuyer.com/news/all-eyes-on-fomc-as-statement-should-offer-inflation-outlook